Banking domain testing has one goal: to keep people’s money safe from software failures.

Everything else is secondary.

A social media app glitch means users get annoyed. A banking app glitch means congressional hearings and federal fines. The difference isn’t just severity—it’s the complete destruction of trust that takes decades to rebuild.

Mobile banking application testing deals with workflows that span 15+ integrated systems, traffic spikes that can crush servers in seconds, and security requirements that would make Pentagon engineers sweat.

A single critical bug can cost millions in regulatory fines, destroy customer trust, and land your company on the front page for all the wrong reasons.

But here’s what makes mobile banking application testing uniquely brutal: you’re racing against competitors while testing workflows that touch 15+ different systems. Traffic spikes can crash everything without warning. Security requirements assume everyone is trying to steal money. Regulations change faster than your development cycles.

So here we will talk about how to test banking domain applications, considering all the factors above.

Mobile banking application testing, new version: August 2025. Prepared by: Igor Kovalenko, QA Lead & Mentor; Michael Tomara, Lead QA Engineer; Maxim Khimii, Automation QA Lead; Sasha Baglai, Content Lead.

Key Takeaways: How to Test Banking Domain Apps

Start with money flows. Test transfers, holds, settlements, card charges, and reversals first. If these fail, users lose money.

Prioritize by financial risk, not feature shine. Map “what happens if this breaks?” and test in that order.

Workflows aren’t linear. Model the full bank application testing process across different modules of a banking system, approvals, fallbacks, and jurisdiction rules.

Test for economic-panic load, not just “high load.” Simulate spikes from paydays, outages, market swings, and promos.

Assume third parties will fail. Use service virtualization and fault injection for bureaus, processors, KYC/AML, and core banking APIs.

Security by default. Threat-model, pen-test, and verify encryption in transit/at rest/in memory. Block OWASP basics before anything else.

Compliance is binary. Prove GDPR/PCI-DSS/SOX with audit-ready evidence: traceability, versioned test artifacts, logs, and approvals.

Real devices win. Cover old Androids, iOS versions, tablets, low RAM, weak CPUs, bad networks, and offline/roaming edge cases.

Accessibility is mandatory. Screen readers, contrast, larger text, focus order, and voice input. Test with assistive tech, not just checklists.

Localization is more than strings. Dates, currencies, cut-off times, holidays, legal notices, and right-to-left layouts must pass.

Write detailed test cases with clear data and corresponding variables in the application. Then add exploratory sessions to break what scripts miss.

Automate the routine, keep humans for the weird. Automate regression, API, data-layer checks, and performance. Keep the UX, risk, and discovery manual.

Test data is sensitive. Use synthetic or masked data, rotate keys, and scrub logs. Never ship real PII to lower environments.

Build production-like environments. Mirror configs, data volumes, rate limits, and network paths. Feature-flag risky changes.

Release safety nets. Kill-switches, rate limiting, circuit breakers, and graceful degradation when partners or modules go dark.

Continuous testing, continuous evidence. Every commit triggers checks; every release produces compliance-ready reports.

Learn from incidents. Feed crash reports, fraud attempts, and failed transactions back into test design.

Final stage of testing isn’t “done”; monitoring is. Watch latency, error budgets, auth failures, and money-movement mismatches in real time.

Culture matters. QA, Dev, Security, and Compliance share one goal: keep people’s money safe. Testing is done to ensure that — every day.

Test for economic-panic load, not just ‘high load’

Paydays, market swings, outage recovery: we model real banking traffic and prove p95/p99 by critical journey.

The importance of banking application testing seems like a no-brainer, given that we all use banking apps and expect a spotless experience. However, when you are about to do any form of banking testing, you need to know why you’re doing it at all. Here are the biggest reasons to invest in testing banking and finance applications:

Facilitating a positive user experience. While using banking solutions is a necessity for many users, they will still choose the most user-friendly application for their financial needs. Testing for the banking domain focuses, among other things, on UI and UX aspects of the solution.

Creating a secure user environment. When using a financial software product, users expect their data to be handled with maximum care, while even the smallest security-related controversy can completely tank the reputation of the business. Extensive QA helps avoid that problem.

Ensuring compliance with industry regulations. The banking industry is one of the most regulated ones, and in addition to the basics like GDPR and ISO/IEC 27001 regulations, there are often new ones introduced by authorities. Continuous testing performed by an experienced team ensures full compliance.

Checking the way different systems integrate. This may not be a fact many regular users are familiar with, but banking & financial solutions often consist of different modules with different objectives. Thorough software testing can verify the correct operation of these modules on their own and as part of a bigger picture.

Maintaining proper performance in every scenario. Like most software solutions, banking apps are prone to spikes in load and other scenarios that are not that easy to account for. However, a seasoned team of QA experts can project every likely and unlikely scenario, making sure your app reacts accordingly.

Challenges In Testing Banking Domain: Road Blocks and Use Cases

Summary: Banking testing faces five critical challenges that occur simultaneously: complex workflows spanning 15+ integrated systems, unpredictable traffic spikes during economic events, third-party dependencies that can fail without warning, diverse device requirements across generations of hardware, and competitive pressure to rush releases.

Unlike other software domains where bugs mean user frustration, banking failures mean financial losses, regulatory violations, and congressional investigations. Success requires planning for all these challenges at once, not treating them as separate problems.

When your software handles people’s life savings, every challenge becomes a potential financial disaster. Here are the five biggest roadblocks that keep banking QA teams awake at night — and why they matter more than you think.

Challenge #1: Intricate business workflows

Banking workflows aren’t simple “click here, get result” processes. They’re intricate webs of approvals, validations, risk assessments, and regulatory checkpoints that span multiple departments and systems.

What makes this brutal:

A simple loan application touches 15+ different systems

Each step has multiple approval gates and fallback scenarios

Workflows change based on customer risk profiles, transaction amounts, and regulatory requirements

Edge cases multiply exponentially with each decision point

Real example: Testing a mortgage application means simulating scenarios like “What happens when a customer’s credit score changes mid-application while they’re in a state with different lending laws, and the property is in a flood zone that just got reclassified?”

Why it breaks testing: Traditional test cases assume linear workflows. Banking workflows are more like choose-your-own-adventure novels written by lawyers.

Challenge #2: User load that breaks everything

Banking apps don’t get gradual traffic growth — they get tsunamis. Market crashes, government stimulus payments, and viral TikTok financial advice can all trigger massive traffic spikes that turn your perfectly functioning app into digital rubble.

Traffic patterns that hurt:

Market volatility: Stock market crashes drive 10x normal traffic to trading features

Payday patterns: First and fifteenth of every month create predictable load spikes

Breaking news: Economic announcements trigger millions of simultaneous balance checks

Holiday shopping: Black Friday isn’t just for retailers — payment processing goes through the roof

Real example: When GameStop stock went viral, trading apps crashed under load they’d never planned for. Users couldn’t buy, couldn’t sell, couldn’t even log in. The lawsuits are still ongoing.

Testing reality: You can’t just test for “high load”—you need to test for “economic panic” load, which is entirely different.

Challenge #3: Complex third-party integration

Banking apps don’t live in isolation. They’re connected to credit bureaus, payment processors, government databases, other banks, and dozens of financial service providers. Each integration is a potential failure point.

Integration complexity:

Payment processors that might go down during peak shopping seasons

Credit bureaus with rate limits that kick in at the worst times

Government systems that run on technology from the Carter administration

Partner banks with different API versions and security requirements

Real-world pain: When Equifax had their massive data breach, it didn’t just affect Equifax — it broke credit checks across thousands of banking applications that relied on their services.

Testing challenge: You can’t control third-party systems, but you’re still responsible when they fail. How do you test for scenarios where your partners become unavailable?

Challenge #4: Endless device diversity

Banking customers use everything from the latest iPhone to Android devices from 2015, tablets their kids dropped, and computers running Windows 7. Your app needs to work on all of them.

Device reality check:

Older devices with limited memory and processing power

Various screen sizes from tiny phones to massive tablets

Different operating systems with varying security capabilities

Accessibility needs for users with disabilities

Network conditions from high-speed fiber to spotty rural connections

Security complications: Older devices often lack modern security features, but you still need to protect sensitive financial data. Testing security across device generations is a nightmare.

Performance puzzle: A feature that works smoothly on a new flagship phone might be completely unusable on a three-year-old budget device.

Challenge #5: Competition

Banking is one of the fastest-growing tech sectors, and that growth comes with pressure. Companies race to market with new features, often cutting corners on testing to beat competitors to launch.

The speed trap:

Feature pressure: “The competitor launched instant transfers — we need them next week”

Regulatory deadlines: New compliance requirements with fixed implementation dates

Market opportunities: Economic changes create windows that won’t stay open

Customer expectations: Users want banking features as fast as they get social media updates

What gets sacrificed:

Security testing gets shortened because “we’ll patch it later”

Edge case testing gets skipped because “most users won’t hit that”

Performance testing gets minimized because “we’ll scale when we need to”

Accessibility testing gets postponed because “it’s not a launch blocker”

Real consequences: Rushing through testing doesn’t just create bugs — it creates security vulnerabilities that put customer financial data at risk. A minor bug in a gaming app means user frustration. A security hole in a banking app means congressional hearings and federal investigations.

The hidden cost: Fixing a security issue in production costs 100x more than catching it in testing, and that’s before you factor in regulatory fines and reputation damage.

Here’s what makes banking testing uniquely challenging: all these problems happen simultaneously. You’re trying to test complex workflows under massive load across multiple devices and integrations while racing against competitors—and if you mess up, people lose money.

The survival strategy: Accept that banking testing is harder than other domains. Plan for it. Budget for it. Staff for it. Because in banking, “good enough” isn’t good enough — it’s a recipe for disaster.

The banks that understand these challenges and build testing strategies around them are the ones that survive regulatory audits, market volatility, and competitive pressure. The ones that don’t become cautionary tales about what happens when you cut corners with other people’s money.

When partners fail, your app shouldn’t

We drill credit bureaus, processors, KYC/AML, and core banking APIs with contract tests and fault injection.

Banking software fails in the most unexpected ways. Here are three wild examples that show how even the biggest financial institutions get caught off guard.

The emoji that broke the bank

In 2016, a customer decided to spice up their account names with emojis — 💸 for “Tax Money” and 🏠 for “Mortgage.” Cute, right? Not for the bank’s systems, which immediately crashed.

The culprit? Legacy character encoding that predates emojis by decades. ASCII and EBCDIC simply don’t know what to do with a crying-laughing face, let alone a house emoji. The same issue can brick Wi-Fi networks and Bluetooth connections — turns out our digital infrastructure wasn’t built for the emoji revolution.

AI makes credit scoring worse

Banks adopted AI to make lending decisions faster and less biased. Plot twist: it made things worse.

AI systems trained on historical data just baked existing biases deeper into the system. Worse, these algorithms now factor in grocery preferences and music taste when deciding if you deserve a loan. And when someone gets rejected? Good luck explaining why — even the engineers don’t know how the AI reached its decision.

So much for transparency.

When HSBC met Black Friday

Even giants stumble. During Black Friday 2018, HSBC’s mobile app collapsed under user load just as millions tried to access their money for shopping deals.

Imagine being locked out of your own bank account during the biggest sale day of the year. The internet was not kind to HSBC that day.

These headline-grabbing failures are just the tip of the iceberg. Banking apps deal with countless smaller bugs daily — the kind that don’t make the news but can still ruin someone’s day. The lesson? Test everything, especially the stuff you think will never break.

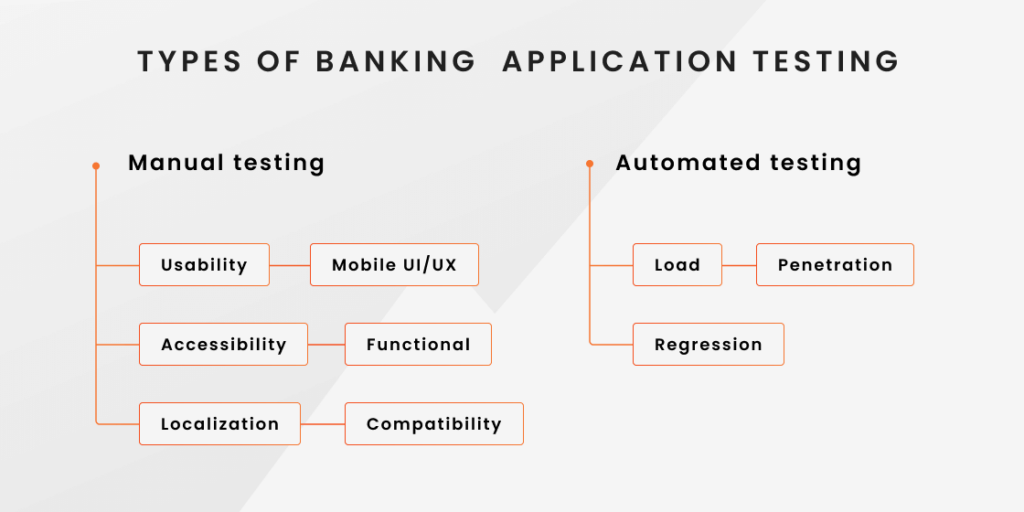

Key Types of Banking Domain Application Testing

Banking applications are typically tested manually and automatically, using a range of testing types to ensure thorough coverage and address the unique challenges of the banking sector. Here’s a deeper look into the key types of banking domain application testing.

Manual banking app testing

Manual banking application testing involves a quality assurance engineer manually executing specific test case scenarios. This allows the development team to evaluate the product from human perspective and improve the subjective side of the application, intuitiveness and aesthetics included.

Usability testing

Usability testing is pretty self-explanatory ― it examines how easy and comfortable it is to use a mobile or web application for different people. Typically, usability testing involves executing standard test scenarios for the app and documenting issues that representative users or manual testers encounter during execution, particularly those related to UI/UX design. The test cases should be realistic, like booking a flight for a customer-facing airport CRM or tracking an order for an online shop. Test case for banking application in this context could vary as follows:

Log in with correct or incorrect credentials;

Check card balance;

Initiate a transaction to another account with valid or invalid data;

Check the status of the transaction.

Mobile UI/UX testing for banking

Due to its sensory and technical peculiarities, mobile application testing differs a lot from desktop and web programs. Mobile banking testing is mostly centered on UI/UX because the basic functionality of such applications are not the easiest to reflect on a small screen. Test case scenarios for mobile UI/UX usually include:

Testing the visual elements in terms of position, resolution, and size;

Testing the pop-up windows and messages;

Testing the readability of app’s content;

Testing the alignment of the buttons, icons, and other elements;

Testing the clickable elements for the comfort of use;

Testing the different screen resolutions and sizes to see if the app looks appropriately on all devices that are planned to cover.

Accessibility testing

Accessibility testing ensures your banking application works for users with disabilities by validating compliance with WCAG guidelines and testing with assistive technologies. This involves testing actual user interactions with accessibility features rather than just checking if features exist. For banking apps, accessibility testing is critical since financial services must be available to all users regardless of abilities.

Key accessibility testing activities for banking applications:

Test screen reader compatibility;

Validate keyboard navigation;

Test color contrast and visual elements;

Verify touch target sizing;

Test with voice control software;

Validate focus management.

Functional testing

A typical banking application has a wide range of features, and the job of the testing team is to make sure they are all present and operate properly in the release version of the product. Functional testing helps engineers focus on the following:

The time needed for the application to launch;

Registration of a new user;

Login of an existing user;

Transactions and cash withdrawal;

Cancellation of a transaction;

Communication with technical support in the app;

Session finalization with a corresponding warning message;

Notifications and pop-ups.

Localization testing

The purpose of localization is to ensure that the content displayed in the application fits the region it is intended to launch in. Due to the cultural differences across countries, the look of the app at times requires drastic changes. Localization testing also ensures that the application complies with local laws and regulations, so it usually goes deeper than just language and timezone settings. Online-banking tests for localization include:

Different default currency for each region;

Time and date change according to the location;

Marketing campaigns adjustment (like congratulatory messages regarding the local holidays);

Translation and switchable multi-language interfaces;

Adherence to the local regulations regarding the finance and tax monitoring.

Compatibility testing

Compatibility testing refers to the analysis of how your application functions with various operating systems, network environments, and hardware models. To test the compatibility of a banking application, software testers usually focus on these specifications:

Networks: Wi-Fi, 5G, etc.

Operating systems, web and mobile: Mac, Windows, Linux, iOS, and Android with defined versions and updates.

Hardware generations: for example, iPhone 6 to 15.

Web browsers: Safari, Google Chrome, Microsoft Edge, Firefox, Opera.

Automated testing

This method of quality assurance is particularly well-suited for routine and continuous testing with strictly defined outcomes (for example, pass/fail criteria or similar). Some types of testing — for example, user acceptance testing — can hardly be automated. However, for many other types, including database testing and integration testing, automation works wonders.

Bank software load testing

Load and performance testing examines the work of an application under different levels of load, from low to average and extremely high. It allows QA departments to prevent application shutdowns because of rapid increase in traffic, as with the HSBC mobile app we mentioned above. To successfully automate bank software load testing, the QA team has to:

Identify critical actions that your application has to perform;

Write test cases basing in these critical actions;

Identify the strict fail/pass outcome for each test case;

Create an isolated test environment that would be free of any traffic other than the results of your load testing;

Let the system execute the test cases and analyze the results.

Penetration testing

Penetration testing is essentially another term for security testing, which assesses the safety and robustness of your system and determines if it’s vulnerable to hacking. The importance of banking applications stems from the fact that they handle all kinds of sensitive information, leaving no room for error.

Track data passed by the application;

Check if any sensitive information is exposed in URLs, binary files, etc.

Identify insecure functions;

Check the application’s reaction to spam attacks;

Monitor proxy server traffic;

Exploit all application’s databases and systems.

Regression banking application testing

Regression application testing is to guarantee that the recent update or a new feature affect the existing codebase of the application. When a developer introduces a code change, even if it was intended at bug fixing, it can interfere with the work of the whole program. When checking a bank app for potential regressions, we recommend paying attention to the following:

Spots and functions that were affected by the last updates;

User-facing features;

Integrations and third-party services.

Learn how we resolved 672 payment bugs with 80%+ success rate across 12 devices for a leading UK fintech.

Benefits of Test Automation in Banking (2025 Playbook)

Summary: Banking test automation delivers controlled risk reduction, automated compliance evidence, and measurable business outcomes. It accelerates releases while protecting money flows, generates audit-ready traceability automatically, validates third-party integrations under failure conditions, and tests for economic-panic loads rather than just high traffic.

The result you can reasonably expect: 30-60% shorter release cycles, 40-70% fewer escaped defects in financial flows, and 50-80% less audit preparation time.

Automation isn’t only faster tests. It’s controlled risk, lower incident rates, and audit-ready evidence. Below is what automated testing in banking should deliver today—and how to measure it.

Release speed with risk under control

Automation accelerates releases without gambling on money flows. Parallel API and data-layer suites catch defects before they hit ledgers. Measure it with lead time, change failure rate, and defect escape.

What it does: Parallel suites on APIs, ledgers, and money-movement flows cut cycle time without gambling on quality. Automate first: transfers, holds, settlements, charge/reversal flows; auth; KYC/AML screens; fees and interest accruals. KPIs: lead time for changes, change failure rate, MTTR, defect-escape rate.

Once speed is tamed, you need proof for auditors.

Evidence on autopilot (compliance that writes itself)

Every run should emit traceability, approvals, and immutable logs mapped to controls (PCI DSS, SOX, GDPR, DORA). Evidence generation moves from manual to pipeline. Audit prep drops from weeks to hours.

What it does: Every pipeline run emits traceability, approvals, logs, and versioned artifacts tied to requirements (PCI DSS, SOX, GDPR). How: link test IDs ⇄ user stories ⇄ controls; sign runs with release hashes; store results immutably. Outcome: audit prep drops from weeks to hours; fewer findings. Testing is also your best audit trail.

Compliance is solid, now harden dependencies.

Third-party safety (because partners fail)

Banks depend on bureaus, processors, core banking, and sanction APIs. Contract tests, version checks, and fault injection validate timeouts, throttling, and schema drift. Fewer outages when partners wobble.

What it does: Contract tests + fault injection for bureaus, processors, core banking, sanctions lists. Automate: timeouts, rate-limit behavior, stale data, schema drift, version skew. Outcome: fewer production incidents when a provider throttles or goes dark.

With integration risk down, protect the data you test with.

Data safety by design

Synthetic and masked datasets model real balances, life-cycle states, and fraud patterns without leaking PII. Rotate keys and scrub logs automatically. Testing is carried across environments without privacy risk.

What it does: Synthetic/segmented datasets model real balances, account states, and transaction graphs without leaking PII. Automate: masking, subsetting, data aging, key rotation in test envs; scrub logs after runs. Outcome: safe banking application automation testing at scale.

Data is safe — now prove you perform under real stress.

Performance that reflects economic reality

Don’t test “high load.” Test economic-panic load: paydays, market swings, promos, outage recovery. Automate spike/recovery, cascading retries, and slow downstreams. Track p95/p99 by journey and error budgets.

What it does: Load models for paydays, market swings, promos, and outage recoveries—not just “high load.” Automate: spike/recovery, cascading retries, downstream slow-downs; device + network shaping. KPIs: p95/p99 latency by journey, error budgets, saturation triggers.

Performance holds; mobile is next.

Mobile is a separate automation track

Mobile banking application testing must run on real devices, weak CPUs, low RAM, spotty networks, roaming, and offline. Automate biometrics, cold starts, upgrades, and secure storage checks. This is mobile banking testing done right.

What it does: Real-device farms run mobile banking application testing across low-RAM phones, older iOS/Android, poor networks, roaming, and offline states. Automate: cold starts, biometric flows, push deep links, app upgrades, secure storage checks (Keychain/Keystore). Use cases:mobile banking testing and mobile banking app testing that mirrors field conditions.

Mobile is stable — lock down the attack surface.

Security checks on every commit

Bake SAST/DAST/IAST, secrets scan, dependency risk, and MASVS checks into CI/CD. Automate token expiry, replay, step-up auth, crypto in transit/at rest/in memory, and root/jailbreak signals. Banking is also about removing exploit paths early.

What it does: SAST/DAST/IAST, API abuse tests, MASVS checks, secrets scanning, dependency risk. Automate: token expiry, replay, step-up auth, cryptography (in transit/at rest/in memory), jailbreak/root detection. Outcome: fewer exploitable paths; faster fixes with evidence.

Secure is good; correct money math is better.

Financial correctness > code coverage

Model-based tests validate fees, FX, interest, cut-off times, and reconciliation across time zones. Assert invariants: money in = money out. Catch rounding, back-dating, and partial failures.

What it does: Model-based tests validate fees, FX, interest, cut-off times, and ledger reconciliation across time zones and jurisdictions. Automate: invariants (money in = money out), rounding rules, back-dated postings, retries after partial failure. KPIs: reconciliation mismatches per release, false-positive/negative fraud rates.

With core flows correct, shift-right safely.

Shift right, safely

Canaries, synthetic monitors, chaos on dark-launched paths, and feature flags reduce blast radius. Rate limiting and circuit breakers stop cascades. Monitor auth failures and money-movement mismatches in real time.

What it does: Synthetic monitors, canaries, and chaos experiments run in production-like or dark-launched paths. Automate: kill-switches, rate limiting, circuit breakers; alert on auth failures and money-movement mismatches. Outcome: faster detection; controlled blast radius.

Now scale the practice without burning teams.

Test case management that speaks “bank”

Tag tests by financial risk, legal control, customer impact, and money flow. Auto-select by risk each release; retire flaky or obsolete cases. Testing is a software testing discipline, but here it maps to regulation and revenue.

What it does: Risk tags (financial, legal, customer), control IDs, and money-flow mapping in your TCM. Automate: selection by risk for each release; aging rules for flaky or obsolete tests. Outcome: focused runs; lower maintenance. Related intent:test case management for banking and automation of testing services for BFSI.

With structure in place, choose what to automate first.

Install, upgrade, rollback — covered

We automate N-2 → latest upgrades, data migrations, and rollbacks. Our suite ensures money paths survive lifecycle changes.

API and message-bus contract tests with third parties.

Data-layer checks and reconciliation.

Performance spikes tied to real events.

Mobile device/network matrices.

Security gates in CI/CD with fail-the-build policies.

Business outcomes you can commit to

30–60% shorter release cycles without higher incident rates.

40–70% fewer escaped defects in money flows.

50–80% less audit prep time due to automated evidence.

>90% coverage of critical negative paths in high-risk journeys.

Testing Strategy Based on Banking Domain Knowledge

When it comes to developing effective test scenarios for banking apps, there are several types of strategies to consider. These scenarios are designed to test different aspects of the app and uncover any potential issues or bugs.

Banking apps test scenarios by type

Positive testing scenarios

Negative testing scenarios

– Logging in successfully with valid credentials; – Making a transaction without any errors; – Checking the account balance and receiving accurate information.

– Attempting to log in with incorrect credentials; – Making a transaction with an invalid account number; – Entering an incorrect PIN code.

Boundary testing scenarios

Exploratory testing scenarios

– Test the edges or limits of the app’s functionality. – Attempting to transfer an amount of money that exceeds the user’s account balance; – Entering a password that is too long; – Trying to input a negative number for a transaction amount.

– Trying different combinations of user inputs to see how the app responds; – Accessing different parts of the app in unexpected ways; – Checking if the app works correctly on different devices or operating systems.

By using a combination of positive, negative, boundary, and exploratory scenarios, QA teams can better identify and remediate any issues or vulnerabilities in banking apps. It’s important to keep in mind that these scenarios are not mutually exclusive and can overlap.

Words by

Michael Tomara, Lead QA Engineer

“In fintech QA, users reign supreme. Assess, refine, and excel – our 2023 approach to ensuring secure, compliant, and user-focused testing for top-notch financial apps.”

Banking apps test scenarios by focus area

Banking apps handle people’s money — which means everything has to work perfectly, every time. Here’s what you actually need to test to avoid becoming the next headline disaster.

UX testing

Performance testing

Usability. Can your grandmother transfer money without calling tech support? If not, you’ve got work to do.

Accessibility. Screen readers, color blindness, motor impairments—your app needs to work for everyone, not just the developer who built it.

Design consistency. Nothing screams “amateur hour” like buttons that look different on every screen. Pick a style and stick with it.

Mobile responsiveness. Your app will be used on everything from tiny phones to massive tablets. Make sure it doesn’t break when someone rotates their screen.

Content clarity. Financial jargon is confusing enough without adding unclear instructions. Write like you’re explaining to a friend, not a lawyer.

Cultural adaptation. “Withdraw” means different things in different cultures. Test across languages and regions—don’t assume your local slang translates.

Stress readiness. Can your app handle Black Friday traffic? Or will you join HSBC in the hall of shame?

Network connectivity. Not everyone has fiber internet. Test on slow connections, spotty Wi-Fi, and that dead zone in the subway.

Scalability. Your app might work fine with 100 users. What about 100,000? Find out before your users do.

Response times. Nobody waits 10 seconds to check their balance. Every delay costs you customers.

Resource usage. A banking app that drains batteries faster than TikTok is a banking app that gets deleted.

Geographic performance. Your servers in New York might be lightning fast, but what about users in rural Montana?

Security testing

Regulatory compliance

Authentication attacks. Try logging in with wrong passwords, expired tokens, and fake credentials. Your security is only as strong as its weakest point.

Vulnerability scanning. SQL injection and cross-site scripting aren’t just theoretical threats — they’re everyday realities. Hunt them down and eliminate them.

Data protection. Sensitive information should be encrypted everywhere—in transit, at rest, and in memory. No exceptions.

Standards compliance. GDPR, PCI-DSS, SOX — these aren’t suggestions. Violating them means fines that can shut down your business.

Data retention. You need to know exactly what data you’re storing, how long you’re keeping it, and when you’re deleting it. “We’ll figure it out later” isn’t a strategy.

Audit trails. When regulators come knocking (and they will), you need logs showing exactly what happened, when it happened, and who did it. Every action, every time.

Banking app testing is about protecting people’s financial lives. Miss a security flaw, and you’re not just dealing with angry customers; you’re dealing with lawsuits, regulatory fines, and front-page headlines you definitely don’t want.

Words by

Maxim Khimii, Automation QA Lead, TestFort

“In 2023, our QA strategy for fintech apps revolves around continuous adaptation and rigorous testing methods to ensure seamless user experiences, regulatory compliance, and unyielding protection against emerging threats in an ever-evolving digital landscape.”

Banking Testing Strategy: Sample Test Cases for Banking Application

Building a testing strategy for banking applications isn’t like testing your average mobile app. When your software handles people’s life savings, every bug could trigger a financial crisis. Here’s how to create a testing strategy that actually works—based on 23+ years of watching banking apps succeed and spectacularly fail.

Step #1: Start with the money-moving features

Skip the nice-to-haves and go straight for the jugular: money transfers, loan approvals, account access, and transaction processing. These are your “break the bank” scenarios—literally.

Why this matters: A broken search feature annoys users. A broken transfer feature bankrupts them. Start with what matters most.

Real example: Test what happens when someone tries to transfer $50,000 at 11:59 PM on December 31st while their account has exactly $50,001. Edge cases in banking aren’t theoretical—they’re Tuesday afternoon.

Step #2: Map the financial disaster zones

Not all bugs are created equal. In banking, some failures mean angry customers; others mean federal investigations.

High-impact areas to prioritize:

Transaction security: Can hackers steal money?

Data privacy: Are account numbers exposed?

Regulatory compliance: Will this get us shut down?

Account access: Can customers reach their money?

Use case example: A login bug might seem minor until you realize it’s preventing millions from accessing their accounts during a market crash.

Step #3: Test with real people, not personas

Banking users aren’t your typical tech-savvy millennials. They’re 78-year-old retirees trying to pay bills and 22-year-old college students checking balances on cracked phone screens.

How to do this right:

Include actual bank customers in beta testing;

Test with users who struggle with technology;

Validate scenarios against real banking workflows.

Reality check: Your perfectly designed user flow might work great for developers but completely confuse the grandmother trying to send money to her grandkids.

Step #4: Automate the boring stuff, keep humans for the weird stuff

Automated testing handles the repetitive transactions. Manual testing catches the bizarre edge cases that only humans think to try.

Integration testing across multiple banking systems.

Test case execution strategy: Automate 80% of your regression tests, but keep humans involved in anything involving user experience or creative destruction.

Step #5: Test early, test often, never stop

Banking regulations change daily. Market conditions shift overnight. Your testing strategy needs to keep up.

Continuous testing in practice:

Every code commit triggers automated security scans;

Daily regression tests catch integration issues;

Weekly user acceptance testing with real scenarios.

Why this saves your skin: The bug you miss today becomes tomorrow’s regulatory violation.

Step #6: Make QA and Dev teams best friends

Banking development moves fast, but mistakes move faster to the front page. Your QA and development teams need to work together like a well-oiled machine.

Tools that actually help:

JIRA for tracking every issue from “minor annoyance” to “federal investigation;”

Daily standups focused on risk assessment, not just progress;

Shared responsibility for security and compliance.

Communication that matters: When a developer says, “It’s just a small change,” QA needs to ask,“ change to what financial regulation?”

Step #7: Use tools that understand banking

Generic test management tools don’t understand the complexity of financial software testing. You need tools that can handle banking-specific requirements.

Look for tools that support:

Compliance reporting for regulatory audits;

Risk-based test prioritization for financial impact;

Security-focused test case management;

Integration with banking systems and databases.

TestRail and similar tools work, but make sure they can handle the complexity of banking workflows.

Step #8: Test based on financial Risk, not feature priority

In banking, risk isn’t about user frustration — it’s about regulatory fines, security breaches, and financial losses.

Risk-based prioritization:

Critical: Features that handle money directly;

High: Security and authentication systems;

Medium: User experience and performance;

Low: Nice-to-have features and cosmetic issues.

Real-world application: Test the fund transfer feature before you test the app’s color scheme.

Step #9: Keep your test cases fresh

Banking regulations evolve. User behaviors change. New attack vectors emerge. Your test cases need to evolve too.

Regular review schedule:

Monthly: Update test cases for regulatory changes;

Quarterly: Review user feedback and adjust scenarios;

Annually: Complete overhaul based on production data.

What to watch: New compliance requirements, emerging security threats, and changing user demographics.

Step #10: Learn from real-world failures

Production data tells you what actually happened, not what you thought would happen.

Data sources that matter:

Crash reports: What’s actually breaking in the field;

User complaints: Where your testing missed the mark;

Transaction failures: What edge cases you didn’t consider;

Security incidents: What attacks you didn’t anticipate.

Action plan: Every production issue should trigger a review of your testing strategy. If users found a bug, why didn’t your tests?

Banking testing strategy isn’t about following best practices — it’s about preventing financial disasters. Every step should be focused on one question: “If this fails, what’s the worst that could happen?”

Answer that question honestly, and you’ll build a testing strategy that actually protects your users’ money and your company’s reputation.

Banking Software Testing: A Step-by-Step Survival Guide

Testing the banking application isn’t like testing your average app. When one full-fledged banking application handles millions in transactions daily, every bug could be a financial disaster. Here’s how to test banking systems for financial transactions without losing your sanity — or your customers’ money.

Stage #1: Requirement gathering — know what you’re building

Before you test anything, you need to understand what “success” looks like. Banking domain knowledge is critical here — you’re not just testing software, you’re testing people’s financial lives.

This phase involves digging deep into what the banking application deals with daily: loan approvals, fund transfers, account management, and regulatory compliance. The requirements gathered here become the foundation for everything that follows.

Pro tip: Banking domain applications have unique requirements that don’t exist in other industries. Understanding concepts like ACH transfers, SWIFT codes, and regulatory frameworks isn’t optional — it’s survival.

Stage #2: Test planning — your battle strategy

After analyzing requirements, QA engineers can get to test preparation and planning. This is where testing strategy meets reality.

Banking application assures financial security, so your test plan needs to cover everything from basic functionality to worst-case scenarios. The QA lead develops a testing strategy that resonates with project objectives and matches the tech stack — documenting everything in checklists and feasibility reports.

What makes banking applications special? Unlike social media apps where a bug means an annoying user experience, banking software’s actions and features directly impact real money. Your test plan needs to reflect these stakes.

Stage #3: Test case design — the art of anticipating failure

Time to write the actual test cases. This is where specification-based, structure-based, and experience-based testing techniques come into play.

For banking applications, we recommend focusing heavily on specification-based testing — every requirement should map to corresponding test case scenarios. The more negative test cases, the better. If a banking application may fail, it probably will.

The three pillars of banking test case design:

Specification-based testing: Does it do what the requirements say?

Structure-based testing: Does the code work as designed?

Experience-based testing: What could go wrong that nobody thought of?

Test cases are derived from real-world banking scenarios. Think beyond happy paths — test what happens when users do the unexpected, systems go down, and Murphy’s Law kicks in.

Not all testing tools understand banking domain requirements. You need tools that can handle:

System integration testing for complex banking workflows;

Database testing that involves testing database objects like transaction logs and account balances;

Black box testing for security and user experience;

Performance testing for high-volume transaction periods.

The modules of a banking application are integrated across multiple systems — your tools need to test these connections thoroughly.

Stage #5: Test environment setup — building your lab

Banking testing environments need to mirror production without the risk. This means:

Separate layer in the application for testing that doesn’t impact live data;

Realistic data volumes that match production traffic;

Security controls that prevent test data from leaking;

Network conditions that simulate real-world usage.

Setting up a proper test environment for net banking applications is like building a flight simulator — it needs to feel real without the consequences of crashing.

Stage #6: Test execution — where theory meets reality

Now comes the moment of truth. Testing ensures that the application works under every conceivable condition.

This software testing procedure involves running through every test case, documenting results, and composing a testing scenario for each discovered issue. The goal is to make sure that the application handles normal operations, edge cases, and everything in between.

Key focus areas:

Functional testing to verify banking features work correctly;

Security testing to protect against financial fraud;

Performance testing to handle peak transaction volumes;

Compliance testing to meet regulatory requirements.

Stage #7: Reporting and closure — Telling the story

The final stage involves documenting everything that happened during this software testing project. This isn’t just paperwork — it’s evidence that due diligence was performed.

Banking applications and the financial industry they serve require detailed audit trails. Your test reports become part of the regulatory compliance documentation that auditors will review.

What makes a good banking test report:

Clear pass/fail criteria for all test cases;

Risk assessment for any remaining issues;

Compliance verification for regulatory requirements;

Performance benchmarks for future releases.

Testing is to ensure that banking systems handle money safely and reliably. Each stage builds on the previous one, creating a comprehensive safety net that protects both the bank and its customers.

Skip a stage, and you risk becoming the next cautionary tale about banking apps that failed when they mattered most. Follow this process, and you’ll deliver banking software that customers can actually trust with their financial future.

From delays to stable releases

Client came in with slips on schedule and security gaps. We cut defects after release, verified behavior under throttling, timeouts, and schema drift, and stabilized cadence in 4 months.

Wrapping Up: Mobile Banking Testing That Protects Money

Banking apps don’t get second chances. Users expect access, accuracy, and security every time. That’s why software testing in banking domain work starts with money flows, risk, and evidence — not features.

The path is clear: model real money movement, test for failure at scale, assume partners will break, secure everything, and prove compliance with audit-ready artifacts. Do it on real devices and in production-like environments. Keep learning from incidents and fold those lessons back into test design. That’s how banking domain testing actually reduces loss and protects trust.

Your next steps

Build a bank-specific test library tied to money flows and regulations. Include test cases for banking application in software testing that cover happy paths, negatives, boundaries, and jurisdiction rules.

Stand up test case management for banking with risk tags, legal references, and evidence IDs.

Plan how to test security for mobile banking application: threat models, device risks, OWASP MASVS, API abuse, crypto checks (in transit/at rest/in memory).

Add banking application automation testing to CI/CD. Prioritize regression, API, data-layer checks, and performance. Scale it as automated testing in banking with clear SLOs and error budgets.

Automate evidence: logs, approvals, traceability, and reports — automation of banking system project documentation should be part of the pipeline, not a manual chore.

If you outsource, you require automation of testing services for BFSI with SLA-backed results and access to raw data.

Treat mobile as its own program: device lab, network shaping, accessibility, localization, and mobile banking application testing side by side with web. Run focused mobile banking testing and mobile banking app testing against old devices, low RAM, and weak networks.

Where we help (pick what you need)

Banking QA audit and risk map (money flows first).

CI/CD enablement for banking application automation testing and compliance evidence.

Mobile security and performance test plan on real devices.

Playbook for third-party failure testing and production-like environments.

Keep it simple: test what moves money, test what can fail under stress, and keep proof. That’s how mobile banking application testing and broader QA keep your app off the front page — and keep customers’ money safe.

Frequently Asked Questions

What makes banking application testing fundamentally different from other software testing?

Banking applications are one industry for which the software testing is used with the highest stakes — bugs can cause actual money loss, regulatory violations, and federal investigations. The characteristics of a banking application include complex money flows, strict regulatory compliance, and multi-system integrations that require specialized domain knowledge. Unlike other apps, where failures mean frustration, banking failures mean congressional hearings, million-dollar fines, and destroyed customer trust that takes decades to rebuild.

Should I use manual or automated testing for my banking application?

Use automation for routine tasks like regression testing, API validation, performance checks, and security scans that have clear pass/fail criteria. Keep manual testing for usability evaluation with real users, exploratory testing of complex workflows, and developing both negative and positive test scenarios that require human judgment about financial implications when you test the application under various conditions.

What should I test first when building a banking application testing strategy?

Start with money-movement features: transfers, holds, settlements, card processing, and transaction reversals. As a domain expert will tell you, domain knowledge is important when prioritizing what to test the application for first — focus on financial risk impact rather than feature complexity. A broken search function annoys users, but a broken transfer function bankrupts them and triggers regulatory scrutiny in this specialized domain of testing.

How do I handle the complexity of testing integrated banking systems?

Focus on testing workflows that span multiple systems using service virtualization for third-party dependencies like credit bureaus and payment processors. When working with any product or application in the banking sector, use contract testing and fault injection to validate behavior when partners fail, and implement comprehensive logging to trace transactions across all integrated components of the financial ecosystem.

What are the biggest challenges in banking application testing, and how do I overcome them?

Major challenges include complex multi-system workflows, economic panic traffic loads, third-party integration failures, diverse device requirements, and strict compliance demands. Overcome these by starting with risk-based prioritization, using real-device testing farms, implementing automated compliance evidence generation, and maintaining production-like test environments that mirror actual banking conditions.

Share:

Jump to section

Hand over your project to the pros.

Let’s talk about how we can give your project the push it needs to succeed!

A commercial writer with 13+ years of experience. Focuses on content for IT, IoT, robotics, AI and neuroscience-related companies. Open for various tech-savvy writing challenges. Speaks four languages, joins running races, plays tennis, reads sci-fi novels.

What makes banking application testing fundamentally different from other software testing?

What makes banking application testing fundamentally different from other software testing?